At a recent Joint Economic Committee hearing, Cato Institute scholar Dr. Adam Michel effectively made the case for pro-growth, neutral tax cuts as a way to stimulate growth in the manufacturing sector and the broader economy. His testimony laid out the economic benefits of immediate expensing, which allows companies to deduct investment costs immediately rather than amortizing them over time.

>>>READ: Congress Advances Bipartisan Bills to Boost R&D, Energy Innovation

At C3 Solutions, we’ve communicated the environmental benefits of expensing. Expensing incentivizes investments in newer, more energy- and water-efficient equipment and technologies. Those investments could include an HVAC system, more energy-efficient lighting, water heaters, insulation, or a new piece of farm equipment that uses less fuel. Companies that have fleets for transportation can invest in more fuel-efficient or innovative technologies for cars, trucks, and planes. In all of these instances, expensing is a win-win-win because it reduces the cost of the initial investment, saves businesses money, and reduces unwanted pollution.

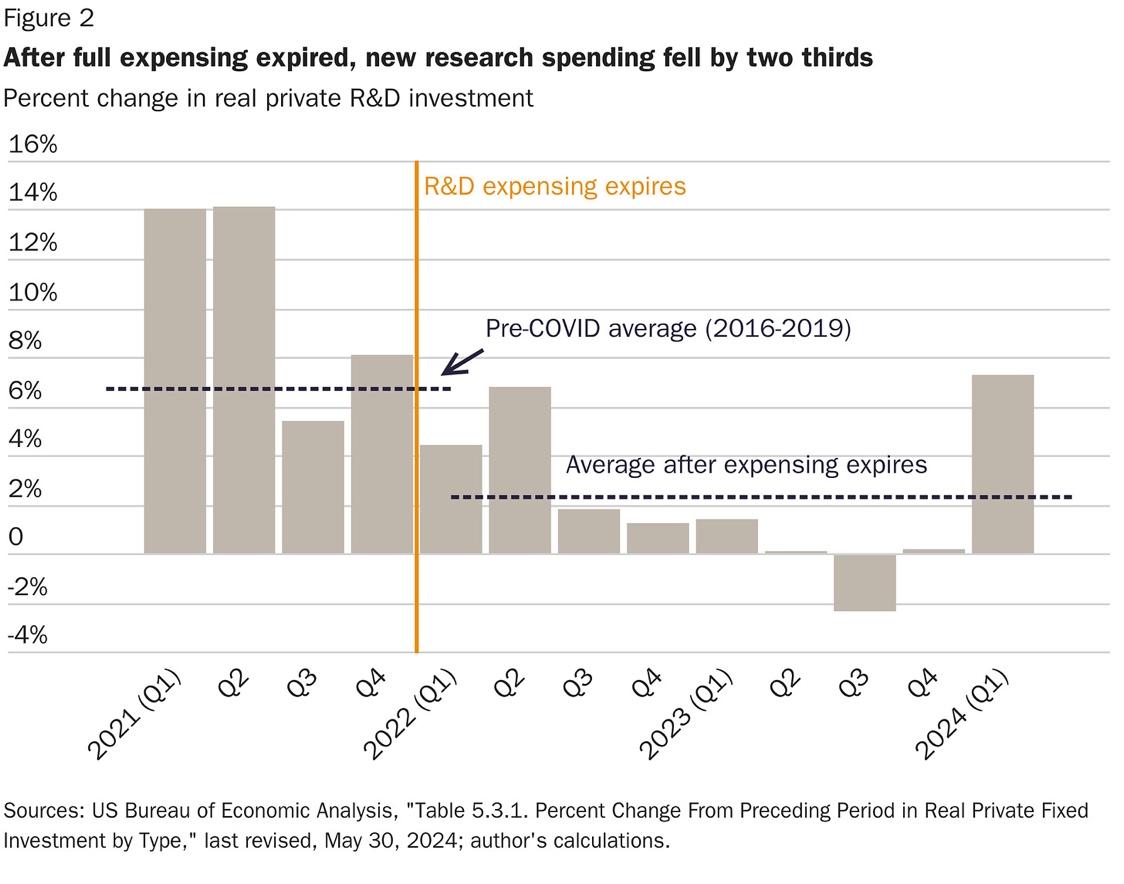

Immediate expensing also accelerates innovation by encouraging investments in research and development. For roughly 70 years, businesses could fully deduct expenses in basic and applied research and development in the year they occurred. The provision covered everything from the wages for scientists and entrepreneurs conducting the research to the cost of equipment, facilities and utilities. That provision lapsed in 2022, meaning companies would have to amortize the expenses over five years. For research occurring outside the country, expenses must be amortized over fifteen years. As Dr. Michel documents in his testimony, the five-year amortization reduces the value of research deductions by about 13 percent. He also shows the adverse impact the tax lapse had on R&D investment in America. Michel writes:

[P]re‐COVID‐19 average quarterly growth rate in real private R&D investment was 6.7 percent and 2021 R&D spending growth was even stronger. Following the loss of full expensing for R&D in the first quarter of 2022, R&D spending growth steadily declined, eventually turning negative. It averaged 2.3 percent through the first quarter of 2024—a 66 percent decline from the pre-COVID average.

No matter what the makeup of Congress and the presidency is, 2025 is going to be a big year for tax policy. Without any action, many Americans and businesses will face higher tax bills as a result of provisions in the Tax Cuts and Jobs Act expiring. That includes a full phase-out of the expensing for short-lived equipment for businesses.

>>>READ: Three Ways Immediate Expensing Helps the Environment

To unlock the full potential of immediate expensing as an engine for green growth, policymakers must recognize the importance of permanence. Making immediate expensing a permanent fixture of the tax code would provide businesses with the confidence and stability needed to undertake ambitious, forward-thinking R&D projects and investments in more energy efficient equipment.

The views and opinions expressed are those of the author’s and do not necessarily reflect the official policy or position of C3.